Stripping the Narrative from the Numbers

If you read Media to Models 1, you might remember our breakdown of “New Homeowner Affordability.” The golden rule is that your total housing cost—principal, interest, taxes, insurance, and HOA fees—should consume less than 30% of your household income.

The media loves to panic over the current national affordability ratio sitting at 32.4%. But mathematically speaking, this isn’t a “crisis”—it is just a structural return to the 50-year historical average of 31%. More importantly, relying on a national average is a massive trap. While coastal markets are heavily burdened with ratios sitting at a brutal 67%, markets right here in Michigan are operating at highly efficient, comfortable ratios between 23% and 30%.

You have probably heard financial commentators and retail lenders advising buyers to “just wait” for interest rates to drop a full percentage point or two before buying. But before you put your life on hold, it is crucial to understand what is actually driving these rates—and why waiting might be a fundamentally flawed strategy.

The Macroeconomic Picture: Spring 2026

Spring 2026 is turning out to be a highly reactive period for the U.S. mortgage market. To understand where interest rates are heading, we have to look at the “Macro Levers”—the external forces like global geopolitics, bond markets, and the Federal Reserve—that dictate the baseline cost of borrowing money.

The Geopolitical Shock and the Oil Factor

The biggest catalyst for the interest rate volatility we saw in March 2026 was the escalating conflict in the Middle East. This pushed Brent crude (the international benchmark for oil) surging past $100.00 per barrel, eventually brushing up against $107.00.

Why does oil matter to your mortgage? Because energy is the foundational ingredient for the global economy. When oil spikes, the cost to manufacture, transport, and deliver goods spikes right along with it. This creates a cascading inflationary effect—and the financial markets are incredibly sensitive to any signs of resurging inflation.

The Bond Market’s Reaction

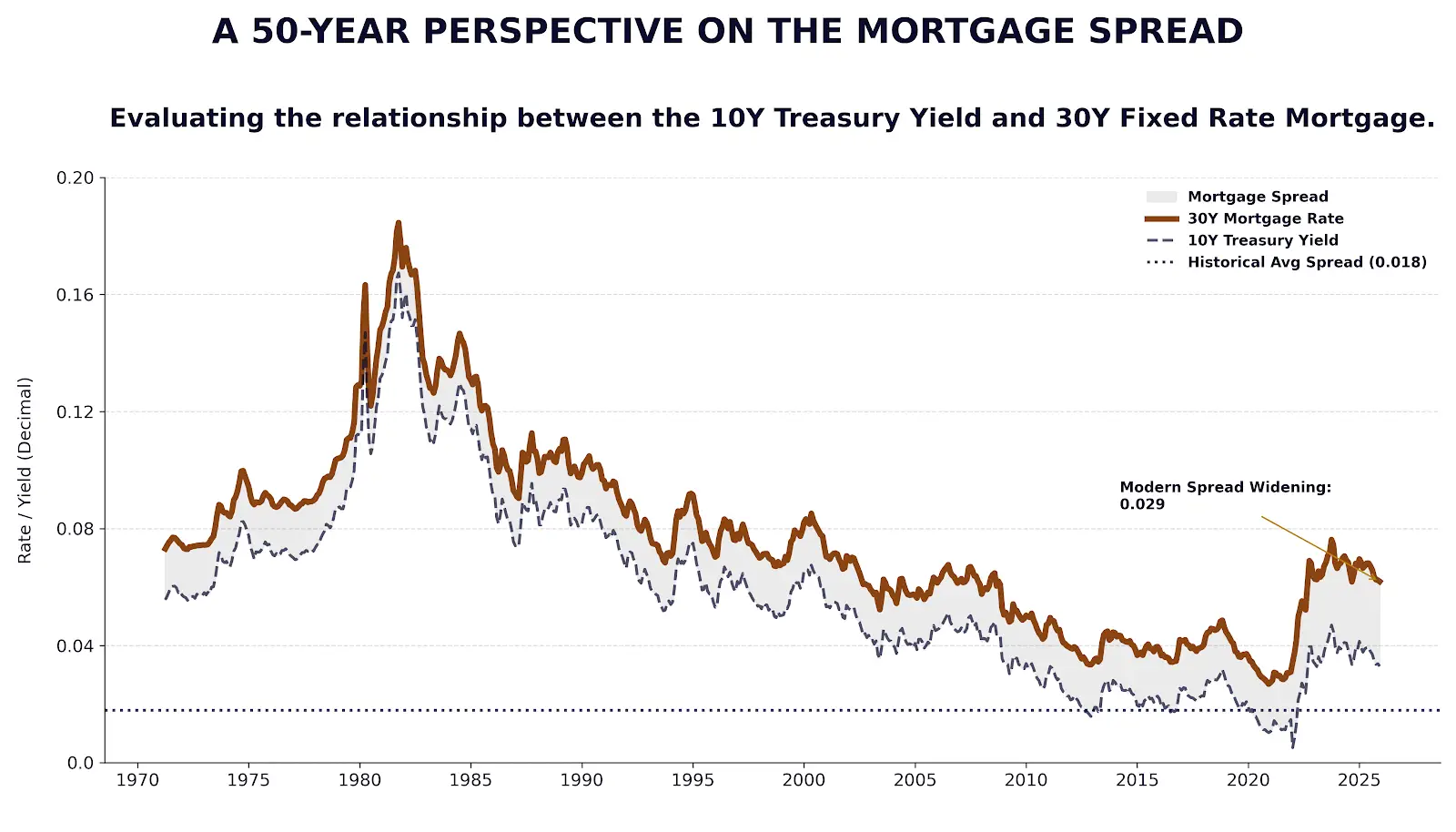

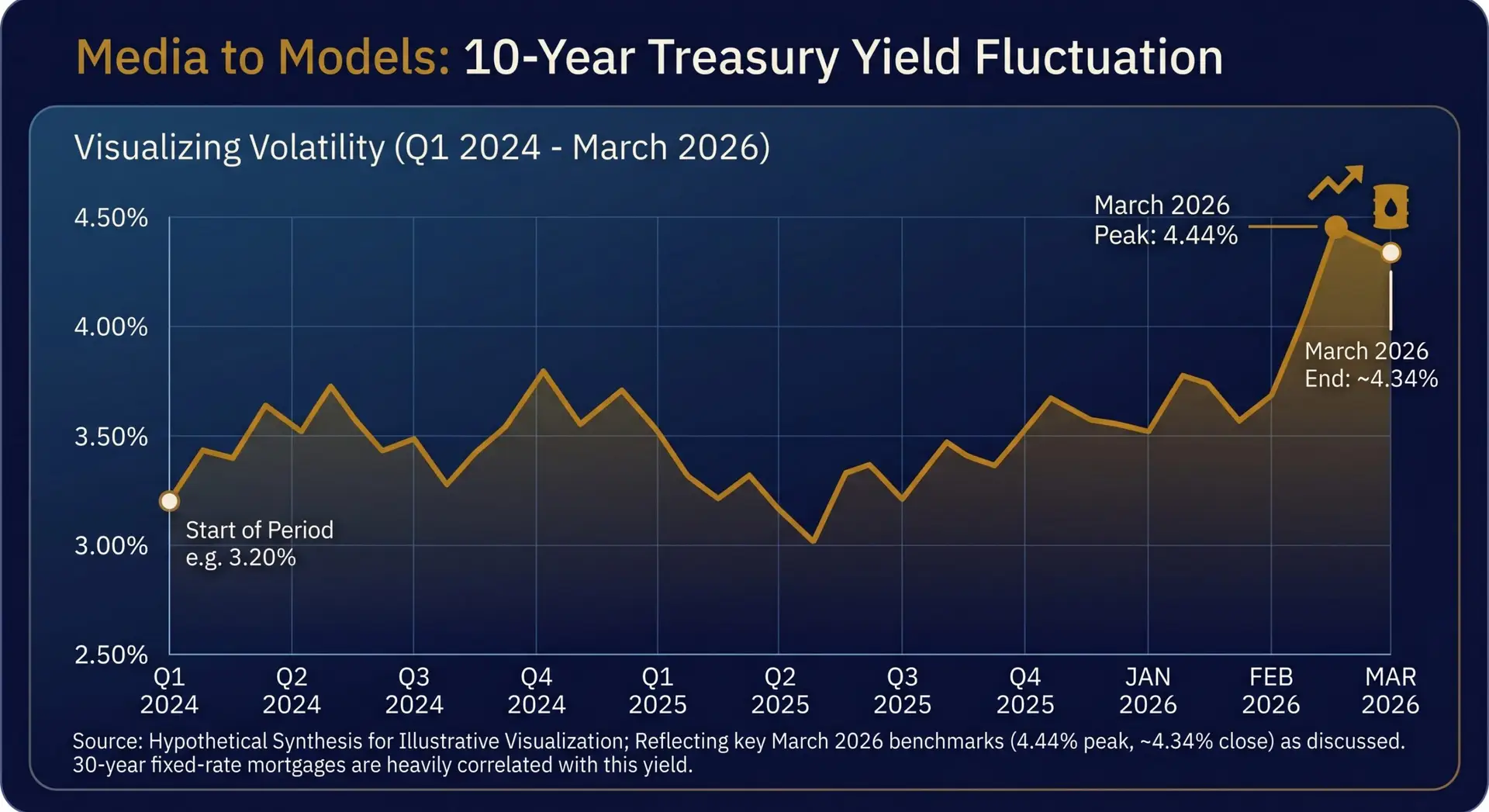

Because of these inflation fears, the yield on the 10-year U.S. Treasury note went for a wild ride. This is critical because the 30-year fixed-rate mortgage is heavily tied to the 10-year Treasury yield. When the Treasury absorbed the oil shock, the yield spiked to an eight-month high of 4.44% before slightly retreating to around 4.34% by the end of March. That rapid bond market fluctuation is the exact reason consumer borrowing costs ticked upward.

The Fed’s Reality Check: The Shifting Neutral Rate

The final—and perhaps most profound—lever is the Federal Reserve. While the Fed does not directly set your mortgage rate, their monetary policy heavily influences the room temperature of the market.

In mid-March 2026, facing down inflationary pressures from the energy shock alongside a surprisingly resilient domestic economy, the Fed unanimously voted to hold their benchmark rate steady at 3.65%. This decision officially slammed the brakes on the rate-cut campaign that optimistic analysts had been hoping for.

So, where does that leave us? The Fed expects the federal funds rate to remain elevated between 3.25% and 3.75% for the rest of 2026. Furthermore, they officially shifted their “longer-run” anchor rate up to 3.0%.

The Bottom Line

In plain English, that anchor rate shift is a watershed moment. The central bankers are signaling that the “neutral rate” of the U.S. economy—the baseline cost of money—is permanently higher now than it was before the pandemic. Mathematically, this invalidates the popular narrative that mortgage rates will eventually drop back down to the historic anomalies of 2.00% to 3.00%. Those days are behind us, and waiting for them to return is no longer a viable real estate strategy.

The Current State of Mortgage Rates

The result of these geopolitical and monetary forces leads to a challenging landscape for borrowers in the spring of 2026. By the final week of March 2026, the cost of capital had officially stabilized at elevated levels.

Extensive market analysis across major national reporting bodies (synthesizing data from sources like Freddie Mac, Bankrate, NerdWallet, and Money.com reflecting consensus averages as of March 26-30, 2026) outlines the finalized environment, particularly validating the conforming 30-Year Fixed-Rate Mortgage which finalized its analysis within a reliable 6.38% to 6.63% (Interest Rate) and 6.39% to 6.68% (APR) range. (While higher variance exists among government-backed products like FHA and VA, these consensus averages represent the definitive market landscape for this volatile timeframe).

Despite this upward volatility, maintaining historical context is critical for perspective: these rates (averaging ~6.5%) remain lower than the definitive 6.65% average observed at the exact same time in March 2025, and are a substantial drop from the punishing 7.00%-plus peak market volatility that dominated late 2023 and 2024. Borrowers are navigating a stabilization–not a crisis.

Forecasting the Horizon: Structural Normalization

While the immediate market conditions are fraught with volatility, economic models and industry forecasts suggest that the latter half of 2026 will bring modest relief, driven by gradual structural normalization. If inflation cools and the labor market demonstrates signs of deceleration, the Federal Reserve may eventually execute the rate cuts that the market has anticipated.

Various institutional models offer differing projections for the trajectory of the 30-year fixed-rate mortgage through the end of 2026:

The consensus among the most robust predictive models is that the interest rate lever will likely settle near the high-5.00% to low-6.00% equilibrium. This realization is critical for homebuyers waiting for a miraculous return to 3.00%. The strategic imperative is to execute transactions based on the objective realities of the current models, utilizing available Micro Levers to force the mathematics in the borrower’s favor. Future improvements can be made through refinancing if miracles happen.

Are You Average?

The media thrives on selling a national affordability crisis. But the spread between a financially strained coast and a highly efficient local market proves that real estate must be evaluated on a hyper-local, zip-by-zip basis. If you aren’t “average,” why fixate on the average headline?

Apply this methodology to your specific situation here: https://thefppartners.com/free-analysis-toolkit

Comments