The Physics of Closing Costs — Modeling Your True Capital Requirements

We hear it all the time – “I’m saving for a down payment on a house.” The media pushes an incomplete narrative that all an individual needs to buy a house is that down payment. They push low down payment options to preview the lowest capital goal possible; however, they neglect to transparently note the true capital needed to purchase a home.

In our previous deep dives, we’ve discussed an assortment of factors that influence price fluctuations related to owning a home. Homeownership is certainly attainable. However, acknowledging that it takes more than the minimum downpayment to achieve is crucial. There is a dangerous gap between a theoretical budget and the physical reality of acquiring the property.

Most buyers are given a strict target for the down payment without being given a true look at what it actually takes to acquire the asset.

This is exactly how conventional real estate thinking operates. A prospective buyer looks at a $500,000 property, calculates a 20% equity requirement, and verifies they have $100,000 in liquidity. The math seems sound. They spend weeks negotiating, inspecting, and planning their transition.

Then, three days before closing, the final paperwork arrives. The document demands $118,500 to actually fund the deal. The buyer is blindsided, scrambling to liquidate other assets or pull favors, and their carefully planned budget is blown apart before they even take the keys.

A math-first, first principles approach prevents this capital shock. We don’t just model the down payment; we model the friction of the transaction and the mechanics of the transfer. To project your true out-of-pocket requirements, you must account for the fully burdened Cash to Close.

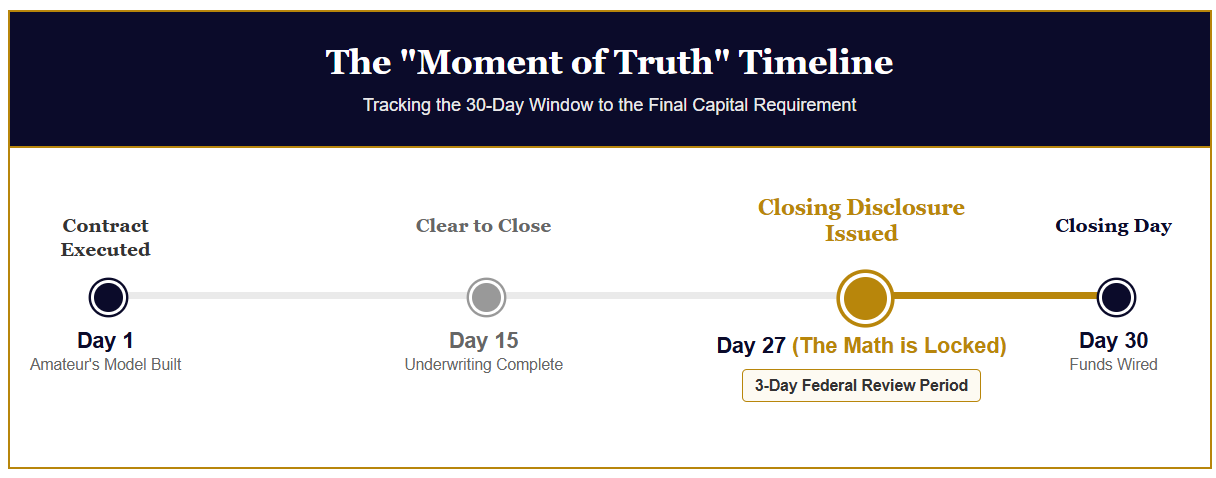

The Timeline of Truth: The Closing Disclosure

The moment of mathematical reckoning in real estate happens exactly three business days before you sign the final paperwork.

By federal law, your lender is required to issue a document called the Closing Disclosure (CD). This is a five-page, standardized form that legally locks in every single variable of your transaction. It outlines your final interest rate, your exact monthly payment, and crucially, the exact dollar amount you must wire to the title company to buy the asset.

If your internal model does not match the CD, your model was wrong.

The Three Vectors of Capital Friction

Closing costs are a collection of fees, taxes, and reserves required by the three primary gatekeepers of your transaction. To model your true out-of-pocket costs, you must quantify three distinct categories of capital friction:

- The Cost of Capital (Lender Fees) If you are using leverage, the bank expects you to pay for the privilege of accessing their balance sheet.

- Origination Fees: Typically 0.5% to 1.0% of the total loan amount. This is the bank’s structural fee for underwriting and processing your debt.

- Discount Points: Optional, upfront capital deployed to permanently buy down your interest rate.

- Appraisal Fees: A non-refundable, upfront cost required by the lender to verify the physical collateral matches the mathematical model.

- Transactional Friction (Third-Party & State Fees) These are the administrative and legal costs required to transfer the asset, clear the title, and record the transaction in the public ledger.

- Title Insurance: The largest single fee in this category. You must purchase a policy to protect the lender (and yourself) against historical claims or liens on the property.

- Recording and Transfer Taxes: Your local municipality charges a tax to officially record the new deed.

- Survey and Environmental: For many properties, verifying legal boundaries and property lines is mandatory.

- Working Capital Requirements (Prepaids & Escrow) This is where incomplete models completely fail. Prepaids are technically still your money, but they must leave your bank account on closing day – they are strict liquidity requirements.

- Property Taxes: Lenders typically require you to pre-fund 3 to 6 months of property taxes into an escrow account to create a safety buffer.

- Insurance Premiums: You must pay for an entire year of property insurance upfront, plus pad the escrow account with additional reserves.

- Per Diem Interest: You must pay the daily interest on your new loan from the day you close until the first day of the following month.

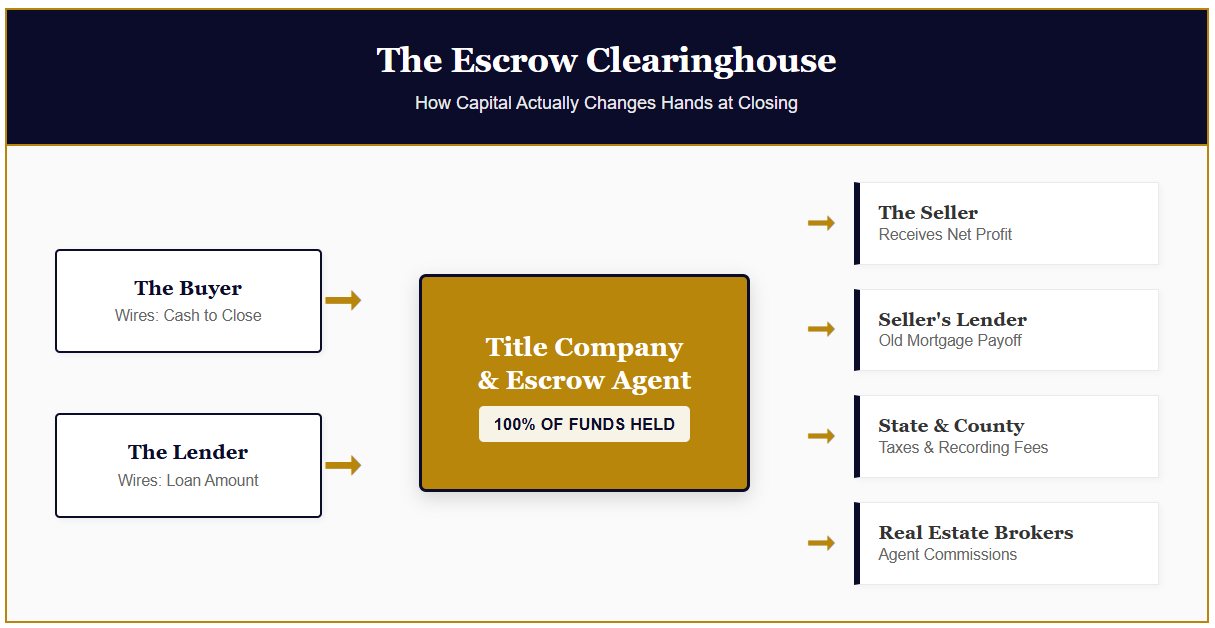

The Mechanics of the Transfer: How Capital Changes Hands

A common misconception in conventional models is that you write a check to the seller for their equity and a check to the bank for their fees.

In reality, neither the buyer nor the lender pays the seller directly. The transaction is facilitated by a neutral third party—the Title Company (or Escrow Agent). They act as the financial clearinghouse for the entire deal.

- The Buyer’s Wire: Based on the final CD, you will wire your entire Cash to Close (Down Payment + Closing Costs) directly into the title company’s secure escrow account. This must be sent as “Good Funds”—meaning a direct bank wire or a cashier’s check. Personal checks are not accepted.

- The Lender’s Wire: The bank wires the remaining 80% of the purchase price into that exact same escrow account.

- The Disbursement: Once the title company holds 100% of the funds, they act as the distributor. They pay off the seller’s old mortgage, pay the real estate agents their commissions, pay the county their taxes, and wire the remaining profit to the seller.

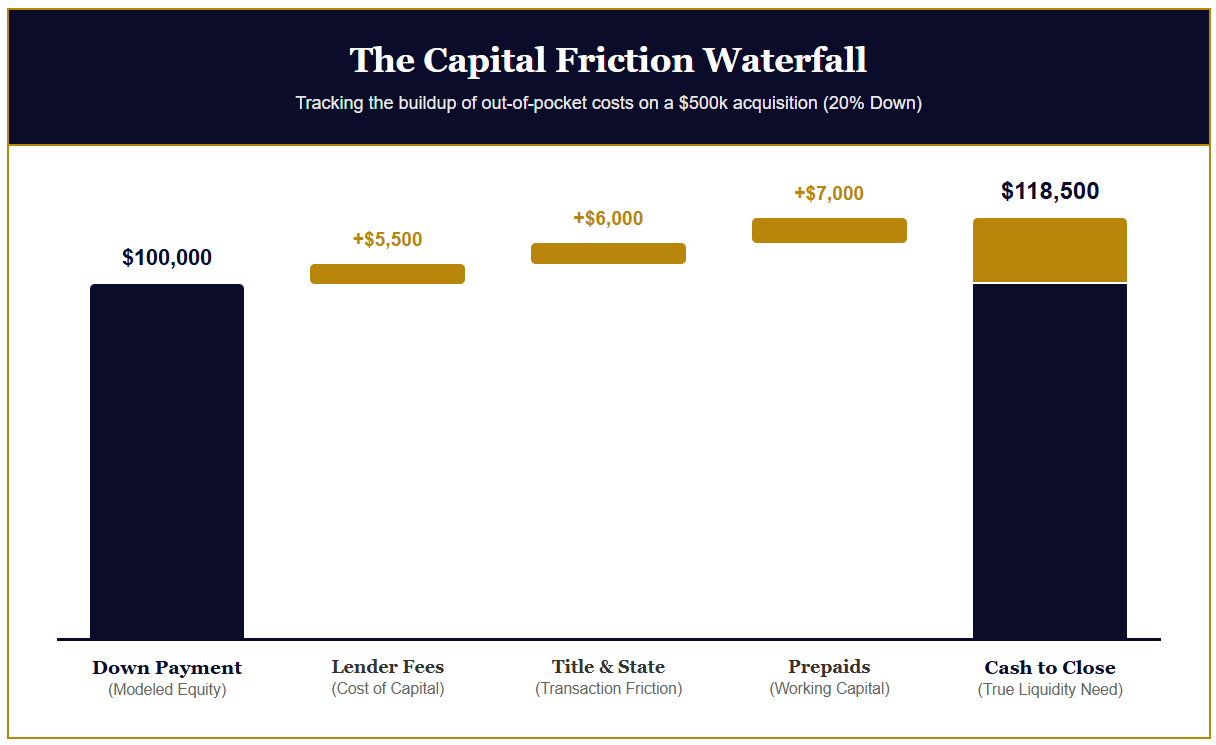

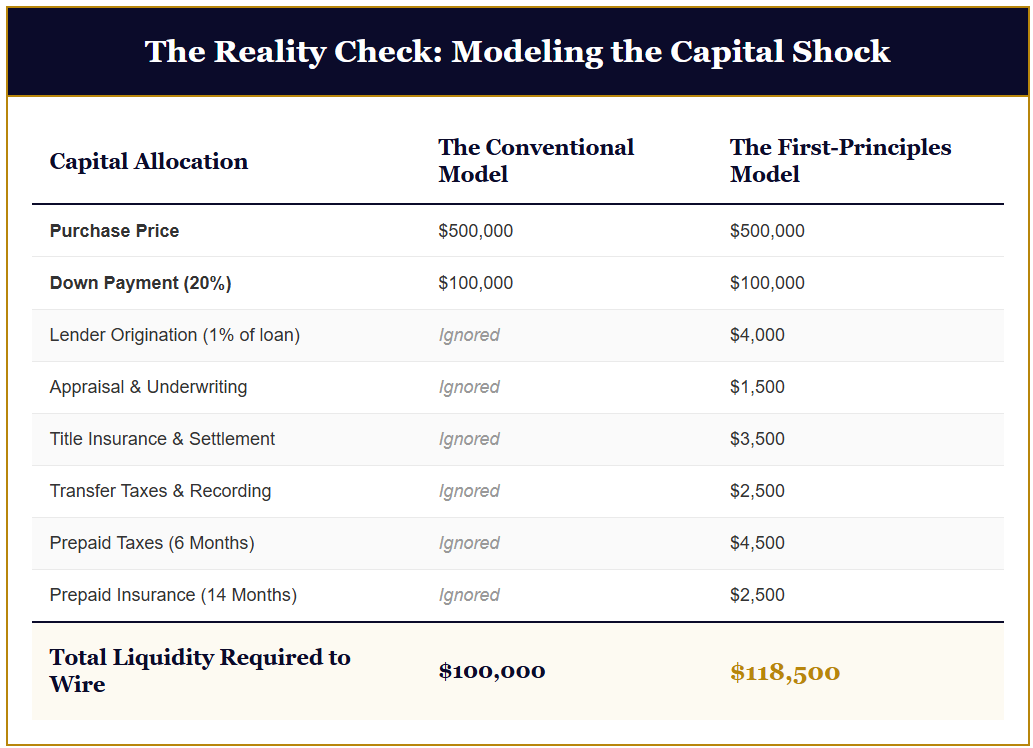

The Reality Check: Modeling the Capital Shock

Let’s look at the mathematical difference between a conventional assumption and a first-principles model on a standard $500,000 acquisition using 80% leverage (a $400,000 loan).

To break this down further:

While the data varies by each unique sale, the conventional buyer in this model faces an 18.5% capital shock when the Closing Disclosure arrives. If your household budgeted exactly $100,000 for this transition, the physical reality of wiring $118,500 instantly drains the cash reserves you had earmarked for immediate repairs, moving expenses, or simply your emergency safety net.

The Bottom Line

A financial model is only as powerful as the physics it accounts for. Stripping out the friction of closing costs isn’t being optimistic; it is mathematically incomplete.

As a general rule of thumb, a rigorous model buffers an additional 2% to 4% of the total purchase price in closing costs and prepaids. It requires more upfront liquidity and forces you to hold heavier cash reserves—but it ensures you are modeling reality, not just best-case scenarios. When that CD hits your inbox three days before closing, your model should already have predicted the exact number on the page.

Are You Average?

The media portrays purchasing a home to be as simple as saving the bare minimum for a down payment, while neglecting the mathematical realities of what it actually takes to close on a home–let alone maintain it. While owning and maintaining a home is a very obtainable goal, your search shouldn’t come with a five-figure surprise. Each home buying process is unique and it needs to be treated as such with a full, transparent look at the data. If you aren’t “average,” why fixate on the average headline?

Apply this methodology to your specific situation here:

Comments